After the Trump-Xi summit, Yassamine Mather starts a discussion on the nature of China and makes a case that Beijing displays the hallmark of an imperial power; a position that will no doubt be controversial for some. Let the debate begin.

At the recent Beijing summit, China’s President Xi Jinping used the language of historical theory to frame the future of relations between China and the United States. By referring to the dangers of the ‘Thucydides trap’,1 he placed the bilateral relationship within a larger frame of whether a rising power and an established hegemon can avoid war and instead build a stable new order.

The message was not simply rhetorical. Xi presented cooperation, mutual respect and restraint as an alternative to direct confrontation, while also making clear that he expected the US to recognise China as an equal global power rather than a subordinate challenger or lesser competitor.

Tesla chief executive Elon Musk, returning from China where he was part of US President Donald Trump’s entourage, was quoted as saying: “What we are going to see with China, for the first time that anyone can remember who is alive, is an economy that is twice the size of the US – possibly three times the size of the US – and it’s going to be very weird living in that world.” The idea captures the scale of the economic shift Washington is trying to manage: China is increasingly being treated as a near-peer economic rival.2

The biggest warning involved Taiwan. Xi implied that peaceful relations depend entirely on how the US handles this issue: if Washington is careful, the relationship stays stable. Trump did not formally alter US policy, but his remarks suggested that Taiwan could become part of a broader bargaining process in a way that has unsettled observers in both Washington and Taipei. The summit did not resolve the Taiwan question: it merely showed that both governments were trying to keep it from exploding in the short term.

In comments after the summit that are worrying the anti-Beijing faction in Taipei, Trump looks like he could break with protocol and talk directly with Taiwan’s President over US arm sales. On Friday, the acting head of the US Navy said the Pentagon would pause arm sales to Taiwan to ensure enough munitions for US operations in the Persian Gulf against Iran.

Economic shadow play and rare earths

The economic side of the summit reflected that same mixture of unresolved rivalry. Both sides announced new mechanisms for managing disputes, including a trade board and an investment board designed to keep dialogue going and reduce friction over tariffs, market access and industrial policy. These bodies were significant, but they were process agreements rather than final solutions. They showed that neither side wanted complete breakdown, but neither was prepared to resolve the deeper structural conflict between them either.

The concrete economic proposals focused on trade and market access. China was expected to increase imports of American goods, especially in the areas of agriculture, energy and aviation. Boeing aircraft, farm products and energy exports featured prominently in the package, though Boeing’s share price fell as the confirmed 200 plane deal was lower than the 500 planes that Wall Street investors had priced in.

Reports also pointed to commitments involving beef and poultry market access, along with renewed or expanded Chinese purchases of US agricultural products over the coming years. These moves were politically useful for both governments, because they allowed each side to claim a win: Washington could point to exports and jobs, while Beijing could present the deals as evidence of stability and pragmatism.

Rare earths and other critical minerals were another central issue. These materials matter because they are essential for high-tech manufacturing, defence systems, electric vehicles and green technologies. The summit was therefore also about supply chains and strategic leverage. China’s role in the global flow of rare earths gives it an important economic weapon, while the United States remained concerned about dependence on Chinese supply. The meeting helped preserve a fragile trade truce, but it did not remove the underlying vulnerability on either side.

Politically, the summit aimed more at stabilisation than at reconciliation. Both sides had an interest in avoiding a direct crisis, and the public language reflected that. Chinese official commentary described the exchange as candid and constructive.

The summit took place against a wider geopolitical backdrop, especially the conflict involving Iran and the Middle East, with Trump wanting China’s help in ending Iran’s closure of the Strait of Hormuz and protecting global energy supplies.

However, Beijing had no desire to bail out Washington or simply follow American priorities. This highlighted a major gap in expectations: the US wanted China to help manage crises fuelled by American pressure, while China refused to act as a junior partner in US strategy.

China’s emerging global role

Ultimately, this meeting was not just about standard trade deals or politics. It was about setting the ground rules for how two rival systems will either live together or end up fighting, in an era defined by tech wars, military competition and a battle for global domination.

This larger strategic context is important for understanding the debate over China’s role in the world economy. China is no longer merely a developing or transitional economy, but an imperialist power operating through finance, infrastructure and trade. From this view, the Belt and Road Initiative (BRI) is not a program of solidarity, but a mechanism for exporting surplus capital, securing influence and binding weaker states into asymmetrical dependence.

Let us start with surplus capital. China produces more capital and industrial capacity than it can profitably absorb at home and it must seek external outlets. Its huge industrial base and financial reserves drive it to export capital abroad through infrastructure and lending.

On the domestic-capacity side, China’s official manufacturing capacity utilisation was 75.2% in the second quarter of 2024, and non-metallic mineral products were only 64.2%, while the Organisation for Economic Cooperation and Development says Chinese steel exports in 2024 exceeded 118 million tonnes and rose because of excess capacity.

Belt and Road has become a way of absorbing overcapacity in steel, cement, heavy machinery and construction, while opening up foreign markets for Chinese firms. Projects are often built by Chinese state-owned enterprises, using Chinese materials, Chinese labour and Chinese finance – which means that much of the value circulates back into Chinese corporate and state structures.

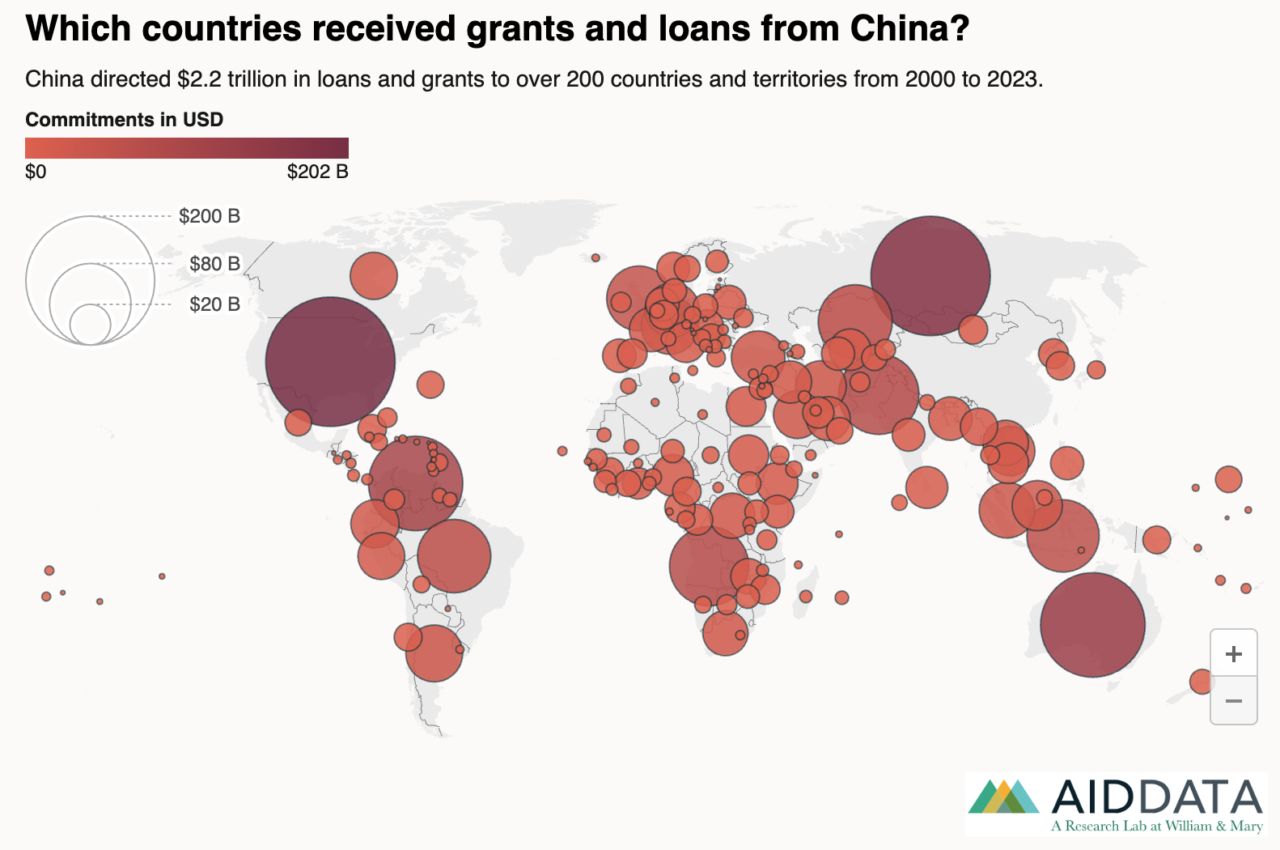

On the capital side, China still had US$3.22 trillion in foreign exchange reserves in June 2024, and the European Central Bank’s Survey on the Access to Finance of Enterprises reported a US$422 billion current account surplus for 2024. China’s ministry of commerce reported US$147.85 billion of outward direct investment in 2023 and US$85.3 billion in all-sector overseas direct investment in just the first half of 2024, while AidData estimates China’s global loans-and-grants portfolio at US$2.2 trillion across 200 countries and says China remains the world’s largest official creditor. When recipient states struggle to repay, China gains leverage over ports, mines, railways or other strategic assets.

The Hambantota case in Sri Lanka is frequently cited in this context, because it is seen as an example of how debt can translate into prolonged control over infrastructure and land. Between 2007 and 2013 Sri Lanka borrowed billions from China to build a massive port in the president’s home district. Facing unmanageable debt in 2017, Sri Lanka leased the Hambantota Port and surrounding land to a Chinese state-owned firm for 99 years in exchange for a US$1.12 billion cash payout. It used this money to stabilise its reserves and pay off other creditors, meaning the original Chinese construction loans were never actually erased.

Another example is Angola. According to AidData, a Chinese loan to Angola was backed by future oil revenues. As oil prices fell, Angola had to use Chinese-controlled escrow accounts just to cover the interest. Montenegro’s Chinese highway loan nearly ruined its national finances, forcing the country to use Western refinancing and hedging to manage the debt. More broadly, the debt structure of Belt and Road agreements gives China influence over policy and assets without the need for military intervention.

Another key argument is unequal exchange. Belt and Road projects often reinforce the existing global division of labour rather than overcoming it. Many countries remain dependent on exporting raw materials, oil, minerals or agricultural goods, while importing Chinese manufactured products and technology. In places such as Africa, Latin America and parts of central Asia, China’s economic model can lock host states into commodity dependence rather than helping them build autonomous industrial capacity. A clear example is sub-Saharan Africa, where China is the largest trading partner, African exports to China are concentrated in metals, fuel and minerals, and Chinese imports are mostly manufactured goods and machinery (in Latin America, Chinese trade and investment have similarly tended to reinforce commodity specialisation rather than broad-based industrial upgrading). For example, in deals with the Democratic Republic of Congo infrastructure construction was traded for long-term mining concessions for cobalt and copper – resources vital for China’s high-tech domestic industries.

Is Belt and Road an alternative or a new imperialism?

A related point is legal and political sovereignty. Belt and Road contracts often contain clauses that protect Chinese investors through arbitration systems, confidentiality rules, waivers that weaken the ability of host states to resist asset seizure in the event of default, often through the China International Economic and Trade Arbitration Commission. In this sense, China is accused of using legal rather than military tools to secure imperial advantage. The absence of open gunboat diplomacy does not make the relationship non-imperialist. It only means that coercion has taken a more modern and financial form. A concrete country example is Zambia, where Chinese lending became central to the sovereign debt crisis and complicated restructuring, because multiple Chinese lenders and contracts had to be negotiated separately.

Supporters of China dispute the above. According to their view, China is not imperialist because the Communist Party (CCP) controls capital, billionaires do not dictate foreign policy, and state-owned enterprises (SOEs) serve national development, not a financial oligarchy. First of all, I would argue that the CCP is an oligarchy, and separating the ‘state’ from the ‘oligarchy’ is a false dichotomy. The state bureaucracy and the CCP elite function as a collective capitalist class. They control capital, accumulate wealth and use state power to expand into foreign markets to secure raw materials and profits, just like Western monopolies. Under Lenin’s definition, one aspect of imperialism involves the export of capital, the rise of monopolies and the scramble for resources. Critics point out that Chinese SOEs behave exactly like transnational corporations: they seek to control supply chains (like lithium in Africa or copper in South America) and exploit local labour to repatriate profits back to the core (Beijing).

Supporters of China’s Belt and Road Initiative argue that it provides real infrastructure that Western institutions such as the International Monetary Fund and World Bank refused to fund. While it is true that the Belt and Road Initiative builds roads, ports, railways and energy grids, this does not mean it develops poor countries in any meaningful or independent way. As explained above, much of this infrastructure is designed around extraction: mines, ports and transport links are often built to move raw materials out of the country and towards China, rather than to integrate and strengthen the local economy. These projects can function as isolated enclaves, benefiting Chinese capital far more than local workers or communities.

The claim that Belt and Road creates local development is also weakened by the way many projects are run. Chinese firms frequently bring in their own engineers, managers and workers, limiting job creation and skills transfer for the host country. Reports of poor labour conditions, environmental damage and restrictions on trade union activity further undermine the idea that Belt and Road represents a progressive alternative to Western-led development.

Supporters of China also dismiss the ‘debt trap’ argument as Western propaganda, claiming that China renegotiates debts and avoids the harsh austerity imposed by the IMF. However, as noted above, even if the idea of a deliberate ‘trap’ is overstated, debt dependency on China can still lead to a serious loss of sovereignty. When countries cannot repay, China can use debt as leverage to demand political loyalty, diplomatic support, access to strategic assets or favourable treatment for Chinese companies. The opacity of Chinese loans, including secret clauses and restrictions on multilateral debt relief, makes this dependency even more dangerous.

The claim that China practices non-interference is also misleading. China may not usually demand regime change in the way the US has done, but it still imposes political conditions. States are expected to support the ‘One China’ policy, cut ties with Taiwan, vote in line with China’s policies at the UN and remain silent on issues such as Hong Kong or politics inside China. This is not genuine neutrality or respect for sovereignty: it is a different form of political pressure.

Overall, the Belt and Road Initiative should not be seen as liberation from Western domination. At best, it replaces one form of dependency with another. As argued above, China’s relations with much of Africa, Latin America and Asia often reproduce the old colonial division of labour: poorer countries export raw materials and import higher-value manufactured goods. This keeps them dependent, subordinate and trapped at the lower end of the global economy. The issue, therefore, is not whether China is better than the West, but whether replacing dependency on Washington with dependency on Beijing can ever be called real development.

Taken together, the summit and the debate around China’s global role reveal a world in transition. The US-China relationship is no longer one of simple engagement or containment: it is a tense equilibrium, shaped by trade conflict, strategic rivalry and mutual dependence. Irrespective of our analysis of China, what is clear is that the country’s rise has altered global power relations, and that both its supporters and its critics see it as reshaping the balance between core and periphery, dependence and autonomy, domination and development.

This article first appeared in the Weekly Worker.

- en.wikipedia.org/wiki/Thucydides_Trap.↩︎

- The total economic output of the US was about US$23 trillion last year, according to the Bureau of Economic Analysis. China’s GDP, meanwhile, was about US$17.1 trillion, according to the nation’s National Bureau of Statistics (moneycentral.com.ng/markets/article/elon-musk-warns-chinas-economy-could-overtake-us).↩︎